Carbon. Removal. Accelerated.

With this motto, our goal is to counter climate change also with carbon removal and negative emissions. carboneer guides your company through carbon markets, negative emissions and climate strategies.

But first things first:

What is Carbon Removal and how does taking CO2-emissions out of the atmosphere relate to global climate goals?

CO2-emissions back at pre-Corona levels

Looking back at the past year, the Corona pandemic will probably be the most remembered thing of 2020. And in the public perception, the pandemic and its effects seem to have displaced climate change as the biggest challenge.

As a result, global energy-related CO2-emissions also fell by about 6 percent in 2020 compared to 2019. Due in particular to lockdown restrictions and the economic crisis, energy-related emissions fell by more than 2 gigatons in 2020 to just over 30 gigatons. No one expected such a drop in emissions in early 2020. In fact, some countries, such as Germany only achieved their climate targets as a result of the Corona crisis. Otherwise emissions would not have dropped that much.

However, a look at the latest figures and statistics reveals that energy-related CO2-emissions have been back at the previous year’s level since December 2020 and could end up just 1 % below pre-Corona emissions of 2019 during 2021.

Carbon Removal essential for climate goals

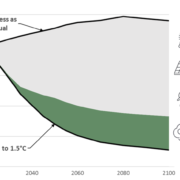

Let’s leave 2020 and 2021 behind for a moment and look at how CO2-emissions would have to develop to meet the Paris Climate Agreement’s 1.5 or 2 degree target. For that to happen, carbon emissions would have to decline globally by about the same factor (3-7 percent) each year for the next few decades as they did during the Corona pandemic.

However, based on the most current plans of the various countries regarding their climate targets (Nationally Determined Contributions), it is more likely that the overall decrease in emissions will be no more than 2 percent by 2030 compared to today. This corresponds to a temperature increase of 2.4 ˚C from pre-industrial levels. Because of these realities, the discussion about large-scale atmospheric removal of CO2 through negative emission technologies is gaining momentum.

Carbon Removal solutions need support

All solutions are needed in the fight against climate change, from emission savings and reductions to the removal of greenhouse gases from the atmosphere. For a process or technology to be considered carbon removal, four conditions must be met:

- CO2 is physically removed from the atmosphere.

- the removed CO2 is permanently stored outside the atmosphere.

- emissions generated during the process are included in the overall balance.

- emissions generated during the process are less than the negative emissions produced.

However, scaling and application of the various nature-based and technological solutions to remove carbon dioxide from the atmosphere are still in their infancy.

Based on scientific research from the IPCC reports, these negative emission technologies will need to remove and permanently store several gigatons of CO2 per year from the atmosphere over the coming years and decades. This is roughly equivalent in magnitude to the decline in CO2-emissions caused by the Corona pandemic, the largest economic collapse since the 1930s.

carboneer: the experts on CO2 markets and negative emissions

Against this background, Simon Göß and Hendrik Schuldt founded carboneer.

Our expertise covers mandatory carbon markets and negative emissions. Through our consulting services (link) we help companies to understand the complexity of carbon markets, to meet the legal requirements and to successfully use negative emissions for the company’s climate strategy.

Feel free to contact us with your questions.

Let’s take the next step towards solving the climate crisis together.

Your team from carboneer.